On December 10, 2018, Citizens for Public Justice was pleased to witness our joint petition with ecumenical partners presented in the House of Commons.

Our petition called on the government to eliminate travel loan repayment for all refugees. This call to action stemmed from our report A Half Welcome, wherein we provided data collected from surveying Sponsorship Agreement Holders (SAHs). One of the major issues SAHs identified in refugee resettlement was the repayment of travel loans, which poses a significant financial burden on newcomers.

Refugees make up 98% of those who utilize the Immigration Loans Program. Already a vulnerable population, for many, the added burden of financial debt can be suffocating.

In response to our petition, the federal government has concluded that there has been cause to make changes to the Immigration Loan Program but not to eliminate it and absorb the costs of travel loans.

This conclusion rests on the basis that 91% of all the loans distributed are repaid. However, this does not take into account the lengths refugees are forced to go to in order to make up this 91% repayment rate. It ignores the stress such a huge financial burden creates on families and individuals and further rejects that any sacrifices are being made in order for refugees to pay back the government. As a result, it appears that the government is profiting off of the suffering of refugees while refusing to see their hardship.

To support our call for the government to eliminate travel loan repayment CPJ interviewed refugees who wished to share stories of how the burden of loans has affected their resettlement in Canada. Hear what they have to say by following #WaiveRepayment on social media.

While listening to their stories, we found trends in lived experiences that indicated further inequities within the system of the Immigration Loans Program.

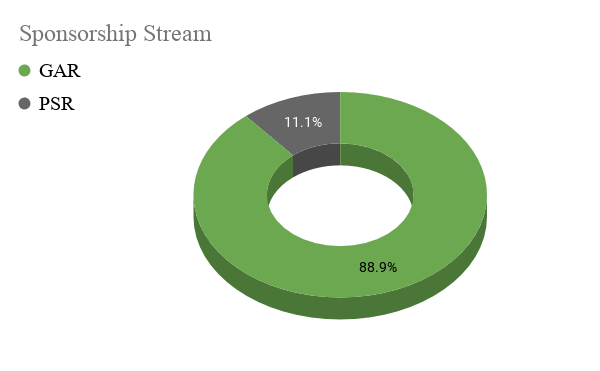

For example, of those interviewed, 88.9% were Government-Assisted Refugees (GARs) compared to the remaining percentage of Privately-Sponsored Refugees (PSRs). This is not a surprising figure given that GARs do not necessarily have the same accessible community-based support system as PSRs do, simply by nature of their method of arrival in Canada.

This reiterates an already well-known problem with refugee resettlement in Canada, being that the bulk of the responsibility rests on private sponsors rather than the government. We see this structurally through the Immigration Levels Plan target numbers for GARs are disproportionate to those of PSRs. Private sponsors in Canada also provide beyond the logistics and financial aspect of resettlement by creating community connections and networks for refugees to successfully integrate with the help of well developed support systems.

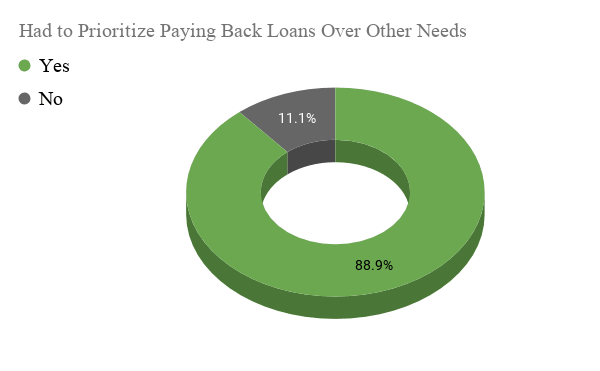

Another unfortunate trend that arose during the interviews we conducted included that the majority of loan holders felt they needed to prioritize paying back the government over other financial needs.

This can include, sacrificing English or French language lessons in order to find work that can immediately assist in loan repayment. Another pattern seen in our interviews was refugees forced to use their income support to repay loans while struggling to determine how they could possibly meet their daily needs. When newcomers are already disproportionately affected by poverty in Canada, this additional burden that the government creates can be extremely difficult to navigate. This is an unfortunate and preventable issue that could be resolved with additional government investment in absorbing the costs of transportation for refugees.

The government has demonstrated that they recognize this burden by absorbing the costs of travel loans for some refugees.

While those facing extenuating circumstances may plead a case to the government regarding their repayment, this is an unnecessary step when it is clear that refugees are already a vulnerable population and the government is simply adding to their burdens.

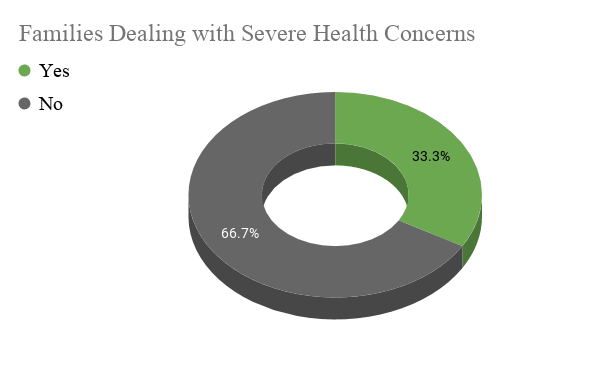

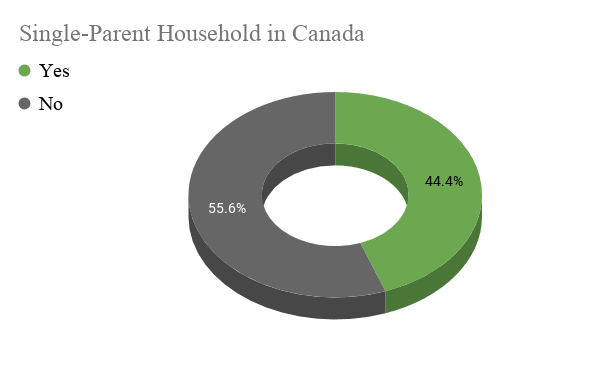

While not representing the majority of the refugees interviewed in our sample, it is also important to note that some of those suffering from extreme health conditions or concerns alongside those who were from single-parent household experienced difficulty repaying their loans.

This further indicates that those who are already disadvantaged are even further marginalized. An intersectional analysis of these refugees specifically, highlights that women are disproportionately affected by these two factors in particular.

Another distinct pattern that occurred during the interviews and caused severe concern was the alarming trend of Black refugees being aggressively told they would lose their status and subsequently become ineligible for permanent residency or citizenship if they were unable to repay their loans.

This is indicative of the anti-Black racism within Canada’s response to refugees that also appears in the rhetoric surrounding irregular border crossings and discrimination based on countries of origin. Unfortunately, this tactic of fear-mongering and threatening Black refugees is unsurprising given Canada’s history of anti-Black racism.

While steps have been taken to reduce the burden transportation loans have on refugees, most recently by making the following changes:

- repayment begins one year after arrival in Canada rather than the 30 days post-arrival

- new loans are interest-free

- existing loans will have no further accumulation of Interest

- repayment extended by two years to reduce the size of monthly installments

Yet, despite these new developments, refugees are still struggling. For many, it is clear that there are little resources for those who wish to plead a case of extenuating circumstances. There remains the possibility that those who are aware have been denied assistance or unable to demonstrate that their circumstances are dire enough for an exception, in spite of these valid lived experiences. Others are simply unable to communicate effectively with the government regarding this issue because of the false threat to their citizenship that has been placed on their shoulders. The premise that lies underneath all of this data is that for the government, the ILP works. They make their money back and through interest, they profit. But at what cost? The rights of refugees ought to outweigh the financial profit.

It’s time to #WaiveRepayment for ALL refugees! Here’s how you can take action:

- Join the conversation by sharing stories of repayment struggles and/or your thoughts and opinions on social media with #WaiveRepayment.

- Tweet at Immigration Minister Ahmed Hussen (@HonAhmedHussen) why you believe refugees should not have to endure the financial burden of loan repayment. (Example: @HonAhmedHussen I believe we should #WaiveRepayment for ALL refugees because ____________).

- Contact your Member of Parliament (MP) and let them know you want all refugees in your community to be treated equitably. You can find out who your MP is and how to contact them by searching your postal code or constituency here.

- Reach out to members of the Standing Committee on Citizenship and Immigration (CIMM) and let them know that refugees and loan repayment must be a priority for the government and that inequities within the system must be addressed to ensure equal treatment of all those to seek refuge in Canada